A part of trading success involves choosing the right broker(s) for your needs. Here’s a list of brokers I currently use, followed by a list of ones I’ve used in the past. I’ll give advantages and disadvantages to each one. I’ll also note that I’m not an affiliate for any of these brokers, so I don’t get anything if you click on the links to them.

Cobra Trading has been my primary broker for a while now. They are an excellent broker if you’re a day trader or short-term swing trader. They are also one of the best if you’re someone who likes to short hard-to-borrow (HTB) stocks like I do.

Advantages

Excellent locates on HTB stocks. If you like to short HTB stocks like I do, then you need a broker with excellent locates. Cobra has 4 locate sources in its platform. Most of the time I’m able to find locates for stocks I want to short. And if there aren’t any locates on the platform, you can call up their chat window to see if one of their customer service representatives can find locates for you.

Direct access. I can route my orders directly to individual exchanges and ECNs, and get rebates if I wish.

Cheap commissions. I only pay 0.003/share for commissions. You can pay even less if you trade really high volumes.

AMAZING customer service. The customer service for Cobra has always been top-notch. It feels very personal, and you almost feel like you get to know the staff there.

Less volatility-related buying power restrictions than other brokers. During the meme stock craze (like AMC/GME), brokers started putting severe buying power restrictions on volatile stocks, and started requiring much higher margin requirements for shorting these stocks. In fact, one reason why I left Vision Financial in early 2021 was due to the extreme buying power restrictions they placed on stocks for shorting, which made it too difficult for me to trade my strategies. I have almost never run into volatility-related buying power issues when trading with Cobra.

No overnight locate fees. Some brokers charge you extra for holding HTB stocks short overnight. The only overnight fees you’ll pay with Cobra are the short interest fees (which you’ll pay at any broker).

Disadvantages

Not for small account traders. You need a minimum of $30K to open an account, and you must maintain a minimum of $25K.

Occasional shorting restrictions on REG SHO stocks. Sometimes you can’t find locates on certain REG SHO stocks, although usually this clears up by the market open. However, you can’t re-use the locates if you get them. If you shorted a REG SHO stock and then covered it, you have to locate new shares if you want to re-short that same stock.

Trading platforms aren’t free unless you trade extremely high volumes. You’ll pay anywhere from $100 – $230/month for your trading platform unless you trade 200-300K shares/month or more.

Centerpoint is also an excellent broker if you’re a day trader. They are also a great broker if you like to short HTB stocks. I primarily use them when I can’t find locates with Cobra, or if the locates happen to be cheaper at Centerpoint. I can’t comment on their customer service as I haven’t interacted with their customer service much.

Advantages

Excellent locates on HTB stocks. Centerpoint has 2 locate sources. Most of the time I’m able to locate something that I want to short.

Discounts for stock locates based on account size. The bigger your account size, the more discount you get. I currently get a 20% discount on my locates. You also get an initial $15 discount on your first locate regardless of your account size.

Direct access.

Cheap commissions. I currently pay $.003/share, and you can pay less if you trade really high volumes.

Recent reductions in the cost of overnight shorts. Centerpoint used to be a poor choice if you wanted to short HTB stocks and hold them overnight. You’d often have to pay 2-4 times your locate fee if you held the shares short overnight. However, this has recently dramatically improved. You can now hold up to 25K shares overnight for free. You’ll pay twice your locate fee for anything over 25K shares. But really that’s not a big disadvantage since most people won’t be holding over 25K shares of something short overnight.

Less REG SHO restrictions. Usually if I’m not able to find a locate for a REG SHO stock on Cobra, I’m able to find one on Centerpoint.

Disadvantages

Not for small account traders. You need a minimum of $50K to open an account, and you must maintain a minimum of $25K.

Trading platforms aren’t free unless you trade extremely high volumes. You’ll pay $120/month for your trading platform unless you trade 200K shares/month or more.

Buying power restrictions on volatile stocks. I’ve had a number of situations where I couldn’t trade with the size I wanted to on certain volatile stocks. When I’d try to do a locate for a certain number of shares, the trading platform would alert me that I’d have insufficient buying power for the shares I was requesting, despite my buying power being sufficient for normal circumstances.

Brokers I Have Used In the Past 4 Years

Here’s some brokers I’ve used in the past 4 years, with some brief commentary on each one. I no longer use them due to them not meeting my needs anymore. Cobra and Centerpoint will likely be my only brokers for the foreseeable future.

TradeZero is probably the best option for small account traders who want to short HTB stocks.

Advantages

Low account minimum. You only need $2500 to open an account, making it ideal for small account traders.

No commissions. You don’t pay commissions on trades. However, commissionless brokers use a pay-for-order flow model, and thus trade execution may not always be the best.

Good locates on HTB stocks. Tradezero has good locates for HTB stocks, making it good for a small account trader who wants to short these stocks.

Rebates on unused HTB stocks that you’ve located. If you’ve located a stock for shorting, and then decide not to use those shares, you can sell them back for a rebate. However, the amount you’ll get back will only be a small percentage of what you originally paid for them.

Free web-based trading platform

Direct access. Tradezero offers direct access to certain ECNs, although the options aren’t as extensive as Cobra or Centerpoint. That means you can also get tiny rebates for adding liquidity to certain routes, although you won’t get the full rebate like you would at brokers like Cobra or Centerpoint (Tradezero will take some of the rebate).

Disadvantages

Steep overnight borrow fees. You’ll pay 4x your locate cost (in addition to the original 1x cost you paid for the locate) to hold a stock short overnight for the first night. It’s then 1x per night each night afterwards.

5K limit per order. If you’re trading more than 5K shares per trade, you need to split them up into multiple orders.

Desktop-based or advanced web platform fee. If you want to trade using the desktop platform or more advanced web platform, you’ll pay $59/month.

Locate fees can be high, although it can vary on the stock. The locate fees you’ll pay at Tradezero can sometimes be higher than Cobra or Centerpoint, although sometimes they’re comparable and there have even been a few instances where it was cheaper at Tradezero.

ETB list is awful. A lot of stocks that are ETB at brokers like Cobra or Centerpoint, including basic largecap stocks like TSLA, are HTB at Tradezero and you’ll have to pay a HTB fee.

Steep Professional Fees for Entities. If you trade through an entity like I do, you’ll pay $300/month in fees.

Paltry rebates for adding liquidity. While you can get a rebate for adding liquidity, Tradezero takes most of it. For example, EDGX provides a .002/share rebate if you add liquidity through it with a broker like Cobra or Centerpoint. However, if you route to EDGX with Tradezero, you’ll only get a rebate of .0005, which is tiny and means Tradezero is taking most of the rebate.

IB has lower account minimums than Cobra or Centerpoint and low commissions making it accessible to small account traders. However, availability of HTB stocks isn’t great, and you can’t reserve shares ahead of time, so it’s not a great broker if you like to short HTB stocks.

Advantages

Option of free or low cost (.005/share) commissions.

Direct routing with low cost (.0035/share) if you choose tiered commission structure, and thus you can get full rebates if you add liquidity to certain routes.

Easy to set OCO (one cancels the other) or bracket orders in its platform Trader Workstation. I always loved IB’s Trader Workstation and the ease with which you could place OCO orders, which is great when you want to have a stop loss and a profit target. I’ve never been able to get OCO orders to work correctly in DAS Trader Pro, which is the platform I use for both Cobra and Centerpoint. I can do “range” orders with DAS, but you’re limited to 2500 shares for an order, so you have to put in multiple orders for range orders in DAS if you have any position more than 2500 shares.

Stops can work premarket and after hours. For most brokers (including Cobra and Centerpoint), stop losses won’t work after hours, so you have to manually watch your trades if you’re trading premarket or after hours. However, in Interactive Brokers Trader Workstation, stop limit (not market) orders can work during premarket and after-hours trading.

Trader Workstation (the trading platform) is free.

Disadvantages

Can’t reserve shares of HTB stocks. With Cobra, Centerpoint, and Tradezero, you can do your locates of HTB stocks ahead of time, pay the fee, and then you have those shares reserved for the trading day. You can then short those stocks and go in and out of them as much as you want (although you can never exceed the amount you initially borrowed…you also can’t repeatedly short a REG SHO stock in Cobra without doing relocating each time). However, in Interactive Brokers, you can’t reserve your shares. Shares will either be available or not at the time you want to trade it. If they’re not available at the time you want to place your trade, well, you’re out of luck. Usually the HTB stocks run out of shares by the time you want to trade them. Thus, IB isn’t a great choice for people that want to short HTB stocks.

$10,000 minimum to open an account. While this isn’t nearly as much as Cobra or Centerpoint, it’s higher than many other brokers, and thus may put it out of reach for some small account traders.

Not great customer service. This is what I’ve heard from others in the past, so maybe it’s changed. During my time with IB, I didn’t do much interaction with their customer service so I can’t comment personally.

Vision Financial was one of the main clearing firms for Centerpoint for a long time before Centerpoint switched to Clear Street. For a while, they had great ability to locate HTB stocks and were one of the best in that area. However, at the time that I had started back up trading in late 2018/early 2019, I didn’t have the minimum funds for a Centerpoint account. Thus, I went to Vision directly and opened an account with them. I was able to get similar borrows on HTB stocks as Centerpoint, although I was under the pattern day trader rule at the time and had to keep close track of my day trades. Because my main strategies involved shorting HTB stocks, my Vision account grew more rapidly (I had opened multiple accounts with multiple brokers to maximize my day trades per week due to the PDT) than the others. In fact, it was the first account of my multiple accounts that eventually exceeded the $25K minimum for the PDT. It became my primary broker for a very long time before Cobra eventually took its place. Unfortunately, I had to leave Vision because they instituted extremely high margin requirements for shorting after the whole AMC/GME debacle. I don’t recall exactly what they were, but it was something like requiring 10x the amount in cash of a stock you wanted to short. So if you wanted to short 1000 shares of a $30 stock, you would need $300K in your account. On top of that, the quality of the HTB locates had deteriorated. I found myself having harder time finding locates in the stocks I wanted to short and for a reasonable locate fee. For these reasons, I left Vision.

Advantages

Low account minimum. When I first opened a Vision account, I only deposited $5000. Thus, it’s a reasonable alternative for small account traders.

Low commissions. When I was with them, I was paying $.005/share.

Better HTB locates than big-name brokers like TD Ameritrade, Etrade, or Interactive Brokers. While the quality of the locates had decreased over time, around the time I left I was still able to get decent locates on a number of HTB stocks through Velocity, their third party locate firm.

No overnight borrow fees on HTB locates.

Direct access.

Excellent customer service. My contact point, Steven Silver, was always amazing and helpful.

Disadvantages

Extremely high margin requirements for shorting. I don’t recall the details, but after the AMC/GME debacle Vision switched its policy on margin requirements for shorts. You now needed something like 10x the cash in your account relative to a position size. Since most of my trades were shorts, this made my strategies mostly untradeable with the size that I wanted to use.

There are many other brokers out there, including some that I used several years ago (for example, I was a Thinkorswim user around 2009-2010…now I only use them for charts). These are the ones I have direct experience with over the past 4 years. There’s a couple others I’ve used in that time frame (Suretrader, TEFS) but they are more sketchy overseas operations and thus I don’t recommend them.

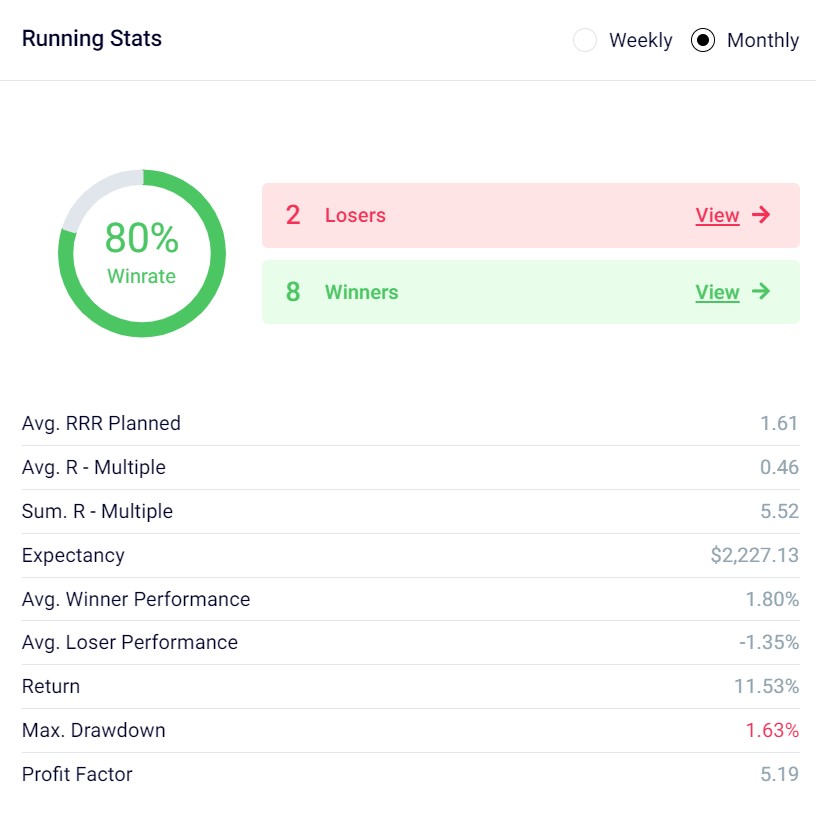

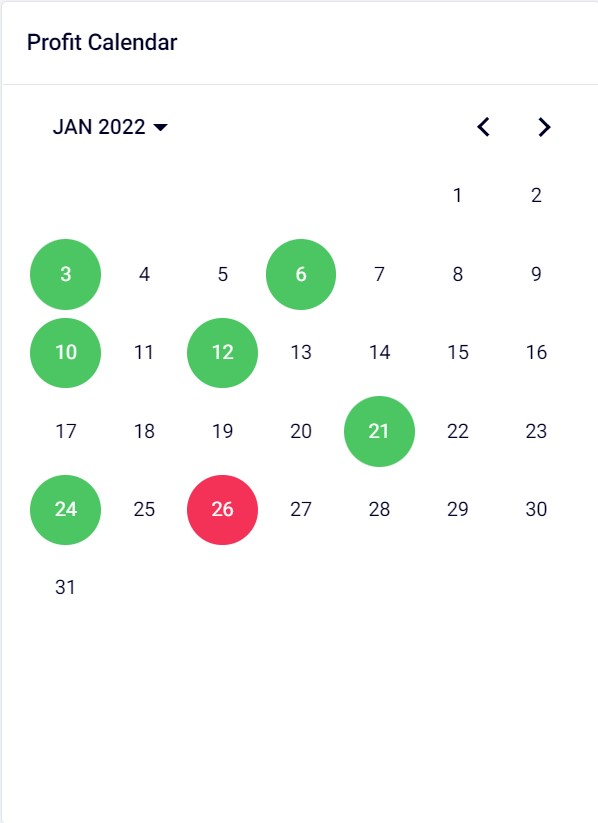

January was a very slow month. The smallcap market, which is the market I primarily trade, was dead. There were very few opportunities that fit within my strategies. I missed some multi-R winners the first week of January. After that, things were just dead…very little would pop up on my Scanz software or on Stockfetcher.

Here’s the stats. I had a high winning trade rate (80%), and only had 10 trades all month. I ended up with +5.5R in profit. While my winning trade rate was high, I didn’t have any multi-R winners. All my winners were +1R or less.

In fact, the smallcap market was so dead that some of my winning trades were from longer term shorts or puts on largecap stocks or funds like TSLA or ARKK.

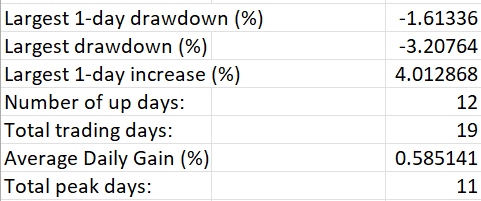

Here’s the stats for my account equity in percentages.

Overall I’m up 11.5% in January, where SPX is down -5.9%. My performance was negatively correlated with the SPX at -0.64 (primarily due to holding longer term large cap stuff…usually I have almost no correlation with SPX in my performance).

Obviously not amazing performance but I did a good job this month of sticking with my known strategies and not experimenting (experimenting too much was responsible for some of my past drawdowns). I’ll continue to be patient. If things continue like this for several months, then I’ll look into developing more strategies.

One thing I’ve learned over the past year is that a lot of people don’t understand money flows and the differences between negative, zero, and positive sum games. If you’re going to invest in any sort of asset, or trade any sort of market, you need to know how money is flowing through it. You need to understand the game you’re playing.

First, to understand positive/zero/negative sum games in the markets, we need to talk about expectancy. Expectancy is very simple…it’s the average profit or loss an investor or trader can expect to make. To calculate expectancy among a group of investors, all we need to do is take their net profit/loss as a group and divide by the number of investors. There will be a net profit if it’s a positive sum game, net zero if it’s zero sum, and net loss if it’s negative sum. Thus, an investor will, on average, make money in a positive sum game, make nothing in zero sum game, and lose money in a negative sum game.

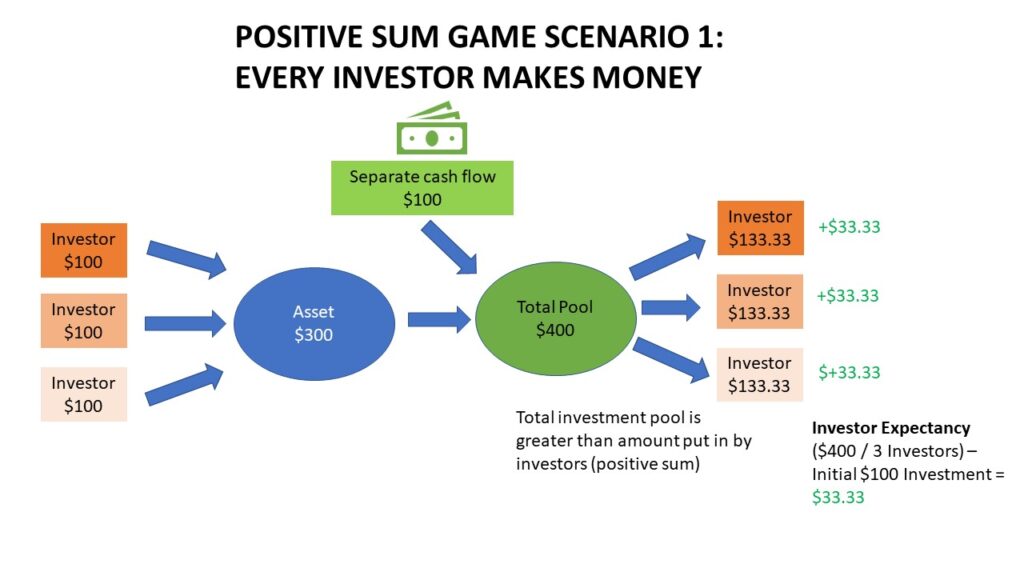

Positive sum game. The amount of money flowing out to investors is greater than what investors put in. There is a net profit. Thus, an investor will make money on average. There is a positive expectancy. That doesn’t mean every investor makes money. Some may actually lose money. It just means that investors make money on average.

Zero sum game. The amount of money flowing out to investors is the same as what investors put in. There is no net profit or loss among the group. Thus, any winning investor is paid out by a losing investor. Even if you have some winners, the expectancy (the average profit) among investors in the group is $0, because the winners were paid out by investors who lost money.

Negative sum game. The amount of money flowing out to investors is less than what investors put in. There is a net loss among the group. While you may have some individual winning investors, the group as a whole has lost money. This is a negative expectancy … investors lose money on average. Any winning investors were paid out by losing investors, but the winning investors didn’t get as much money as was originally put into the system.

Now, let’s get into each type of game in more detail. In each game, I’ll outline a hypothetical system of 3 investors, and show how money flows among these investors. I use a small number for ease of illustration…obviously in the real world we’re dealing with millions of investors. But the number of investors is irrelevant…the mathematics of the money flow remain the same whether you’ve got 3 investors or 3 million investors. I’ll then go over some real-life examples.

Positive Sum Game

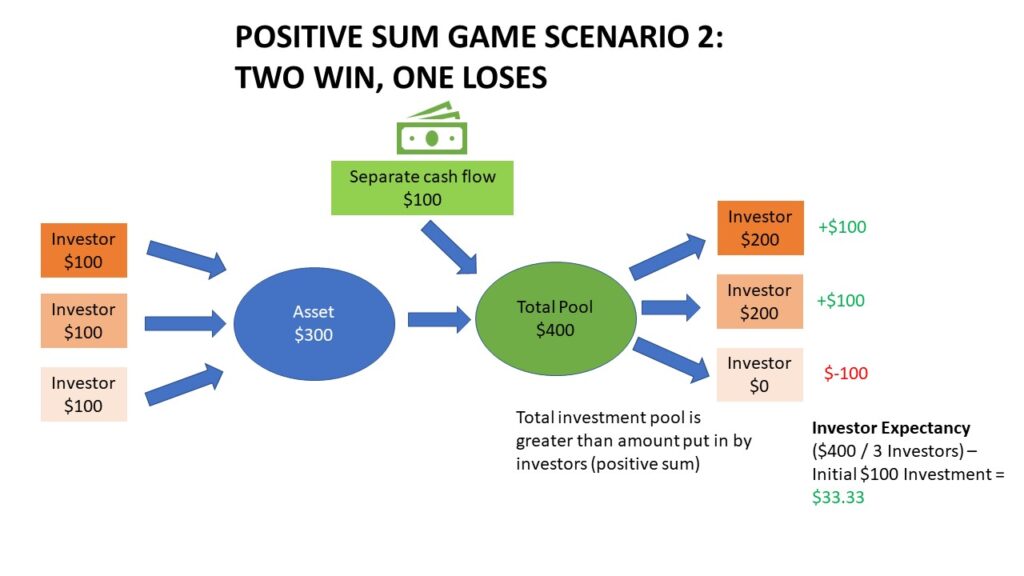

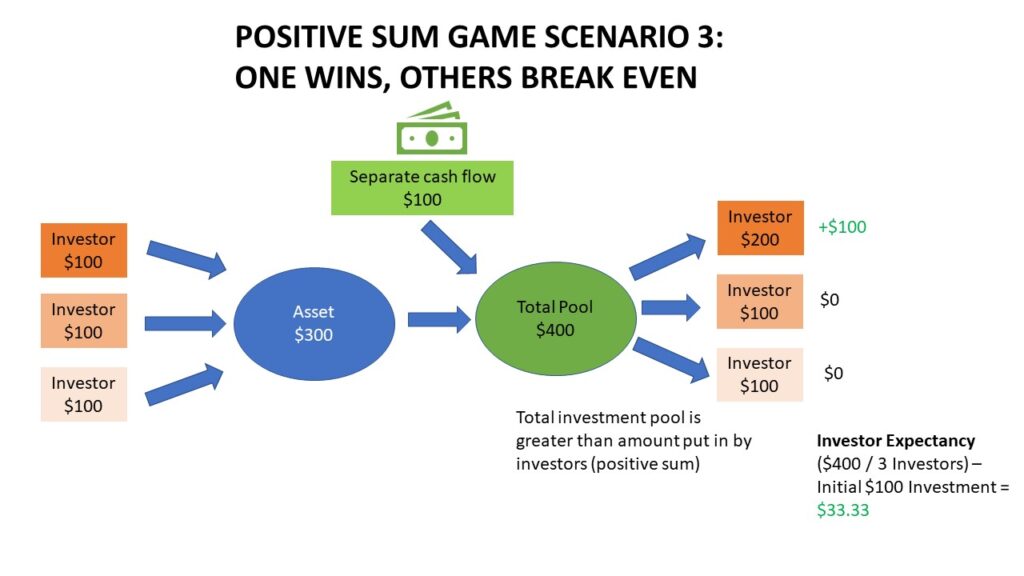

Three investors each put $100 into an asset. Thus, the pool of investment money that’s gone into the asset is $300. The asset also has a separate cash flow (not new investor money) that can go into the asset. Let’s say that separate cash flow is $100. Thus, now the total pool is $400. The total pool is greater than the money that investors put in, making this a positive sum game for investors. The expectancy of the investors in this scenario is ($400 / 3) – initial investment of $100 = $33.3. This is a positive expectancy.

Now, that doesn’t mean every investor makes $33.30 here, or even makes money at all. This is just an average profit. One investor might end up taking $200 from the pool (thus making $100 and giving him a 100% return on his initial investment), while the others only get back $100 and thus don’t make money on their investment. Or, perhaps one investor ends up taking $150 (50% return), and the others end up taking $125 (25% return of each). Or, perhaps one investor takes $300, and the others only get $50. Thus, one investor wins and the other two lose $50 each. But regardless, the average profit is positive.

The key aspect of any positive sum game is that you have money coming into the system that is not new investor money. There are separate cash flows, and investors aren’t just paid out by other investors.

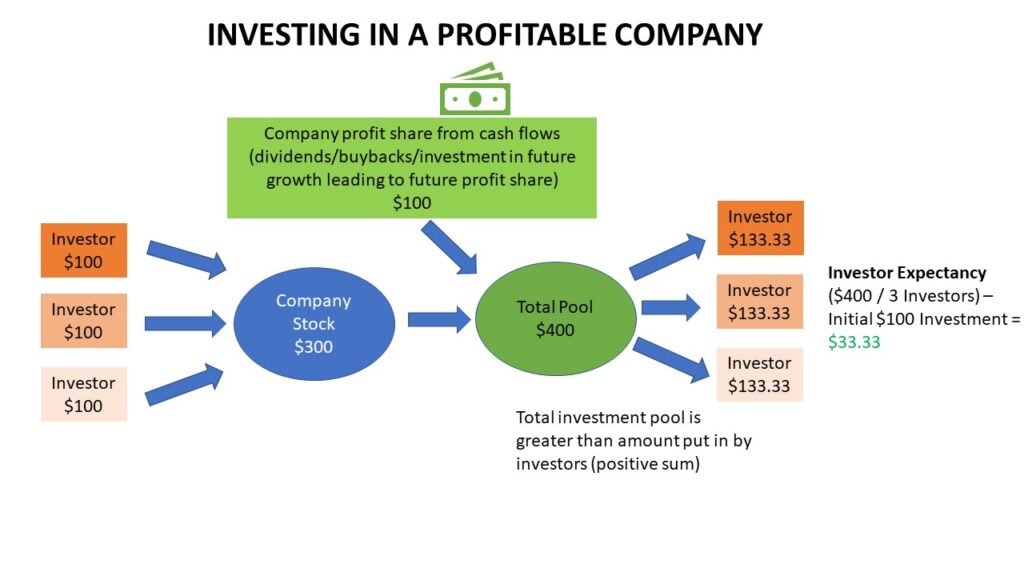

Real Life Example: Investing in a Profitable Company

Investing by buying shares of a profitable company can be an example of a positive sum game. When you invest in a profitable company, you are purchasing the right to a portion of that company’s profits. The company can then share their profits with you in the form of a dividend. Thus, you can make money without having to sell your stock to a “greater fool“. You don’t need new investor money to come in.

A company can also use those profits to buy shares back, which is ultimately returned to you, the shareholder, in the form of share price appreciation (same demand, lower supply = increased price).

A company can also use those profits to expand its operations, leading to growth and future profits, which can then be shared with you down the line.

Note I’m only talking about the game here in terms of investors. Given that companies hire and pay employees with their cash flows, who then turn around and put that money into the economy, there’s more people that benefit other than just investors. There’s a positive sum game in terms of the overall economy. A profitable company also puts out a product that people want and use (this is why they’re profitable!), and thus provides a non-economic net benefit and can be considered a non-financial positive-sum game.

Real Life Example: Investing in Index Funds

This is really just an extension of investing in a profitable companies. Now, you’re just investing in a large group of companies simultaneously. Many of those companies pay dividends. They also all hire employees and are part of the entire economy. They tend to grow with the economy and the overall population. Now, that’s not to say that the overall stock and bond market is always tied to the economy. You can have stock market bubbles where things can get detached from reality and economic output (like the NASDAQ bubble in 1999, or the recent bubble in tech stocks), and the game becomes more zero sum. And actions by the Federal Reserve can impact how the stock market relates to the economy (such as how quantitative easing can influence stock market prices). But overall, over very long periods of time, the overall stock market tends to be a positive sum game, with a positive expectancy for the average investor.

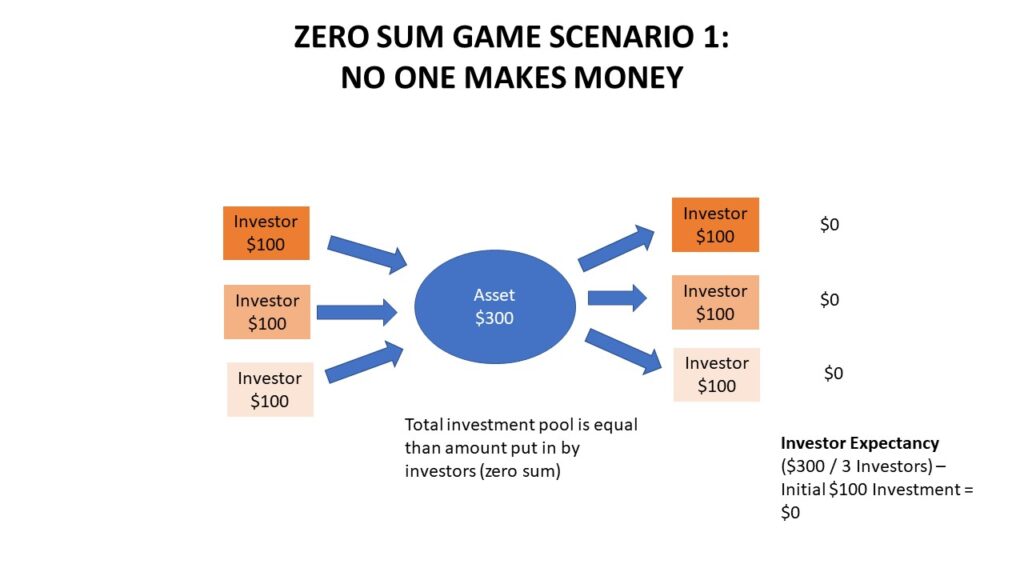

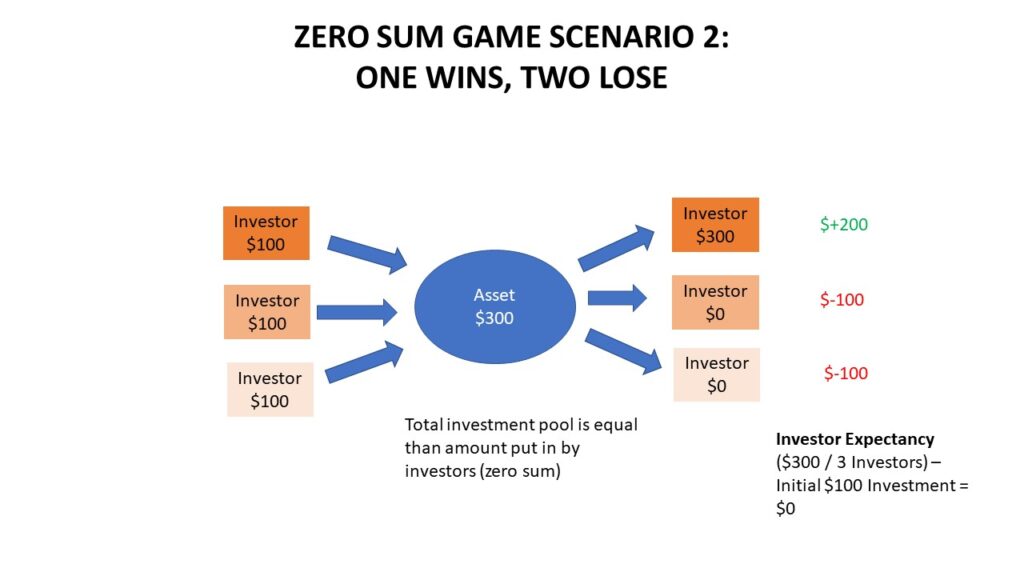

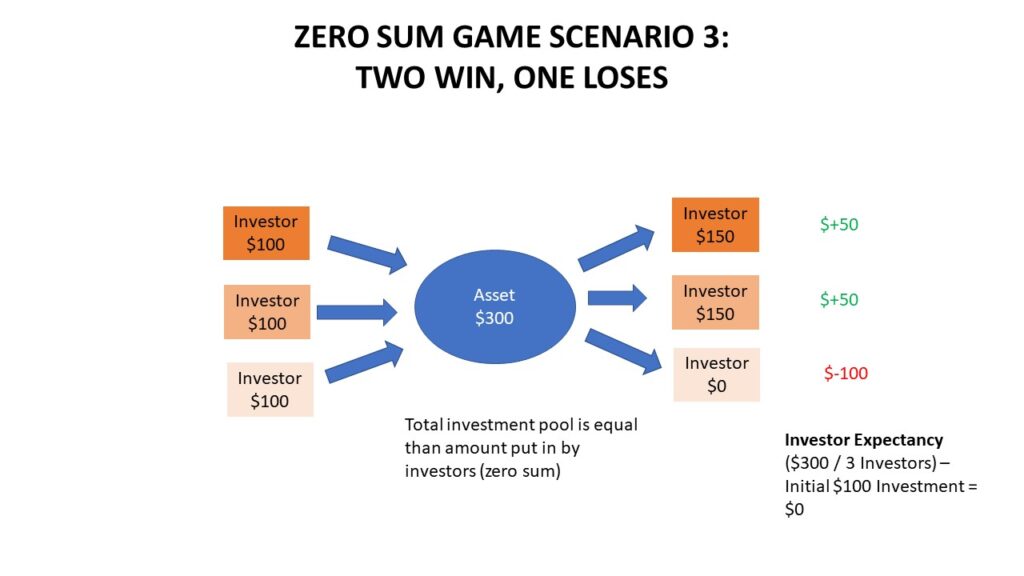

Zero Sum Game

Three investors each put $100 into an asset. Thus, the pool of investment money that’s gone into the asset is $300. There is no other source of money inflows. There is only $300 total available to all the investors. The amount of money that can come out is the same as the money that went in. This is a zero sum game.

The expectancy of the investors in this scenario is ($300 / 3) – initial investment of $100 = $0. This is a zero expectancy. The average investor will not make or lose money. Any winners must be paid out by losers. For example, one investor might take $300 out of the pool (making $200 off his initial investment), while the other two lose $100. Or two investors take $150 each (making $50 off initial investment), while one loses $100.

Real Life Example: Poker

While poker is not an example of an investment, it’s one of the easiest illustrations of a zero sum game. Each player puts money in the pot. One player ultimately wins the money from that pot. The other players lose. The winning player is paid out by the losing players. The amount of money that came out of the pot is the same as the money that went in.

Real Life Example: Day Trading

Day trading is a zero sum game. Any money that one trader makes is money taken from other traders. For example, all of the money I’ve made through day trading is money I’ve taken from other traders. I’m basically a professional poker player playing a giant game of poker with thousands of other players. We are all competing against each other to take each other’s money. This is why, despite numerous requests, I’ll never teach my exact trading strategies to others. I would simply be giving away my edge and giving someone a better ability to take my money. This is also why you should be wary of anyone who is trying to sell a specific trading system. If the system works so well, why would that person be giving the edge away? Most likely the system doesn’t work well and the person is just trying to make money off of selling education systems or off of subscribers. The best trading educators teach general concepts (like InvestorsUnderground), but ultimately leave you to do the hard work of getting the specifics. And no matter how hard you work at day trading, you may not be successful. Since it’s zero sum, not everyone can win no matter how hard they work. Statistics show that most day traders lose money, and less than 1% can consistently make money over the long run. This is why I usually steer people away from day trading despite my own success with it. And if, after all these stats, you still want to be a day trader, make sure you read Michael Goode’s excellent series on it.

Real Life Example: Bubble Assets/Unprofitable Companies/Meme Stocks

Investing in any bubble asset, unprofitable company, or meme stock (like AMC or GME) is going to be a zero sum game. Since the underlying cash flows of the company are insufficient to help pay out investors, the only way for an investor to make money is to sell the asset to a “greater fool.” Thus, one investor’s gain is another investor’s loss. For example, anyone who made money on AMC by cashing out when it had skyrocketed well above 20 was paid out by people who bought the stock at those high prices and are now sitting negative on their investment. In fact, AMC insiders like the CEO made nearly $1 billion dollars by selling into the retail frenzy.

So you know who’s down nearly $1 billion now? That’s right, all of those retail bagholders who bought into the frenzy. The only thing they got out of it was an NFT of a medal.

This is why you should be wary of when you hear about people who made money on some bubble asset like the recent meme stock craze. Anyone who made money was paid out by losers. However, due to survivorship bias, you usually only hear about the winners. It can make it seem like investing in these bubble assets is a good idea, especially when you see the skyrocketing prices. But you don’t hear about all the losers. A similar thing happened with the 1999 tech bubble. You’ll hear about people who made fortunes during that time. But you don’t hear about the massive amounts of people who lost fortunes during that same time. If you want to read some interesting stories of people who lost a lot of money during that time, check out these tweets from @mailboxymoney6 here, here, here, and here).

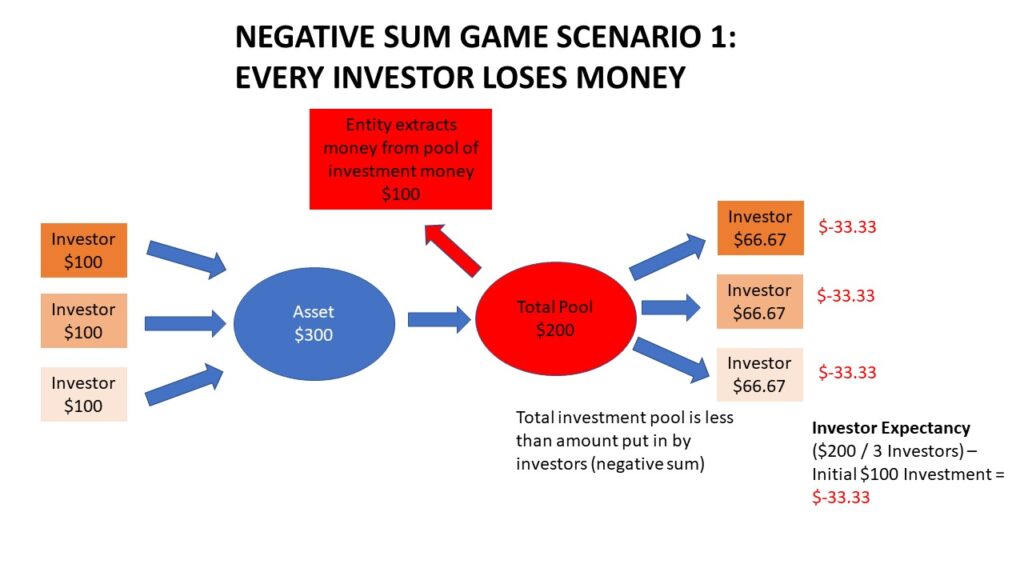

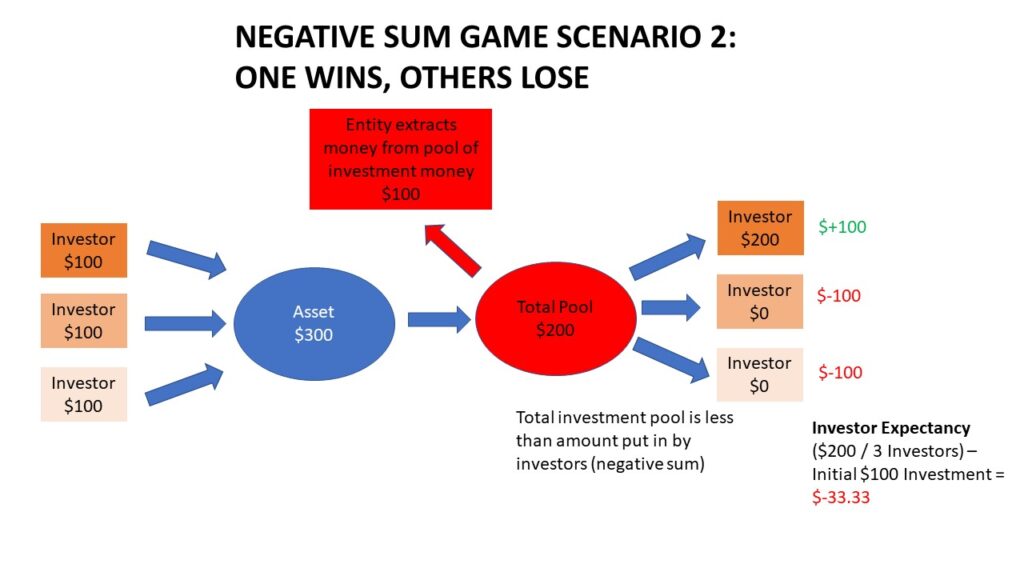

Negative Sum Game

Three investors each put $100 into an asset. Thus, the pool of investment money that’s gone into the asset is $300. There is no other source of money inflows. There is also an additional source of outflows other than investors…a non-investor(s) taking money from the asset. Let’s say this non-investor takes $100 from the pool. Now, the pool of investment money that is available to investors is $200. That’s $100 less than the total money that was put in. Investors as a whole can only be paid out less money than they put in. This is a negative sum game.

The expectancy of the investors in this scenario is (($300 – $100) / 3) – initial investment of $100 = -$33.33. This is a negative expectancy. The average investor loses money. Now, that doesn’t mean everybody loses money. Like a zero-sum game, you can have winners paid out by losers. But even though you may have some winners, the average investor loses. For example, one investor might take the remaining $200 out of the pool (making $100 off his initial investment), while the other two lose $100. You have more losing investors than winning investors in a negative sum system.

Negative sum investment games generally aren’t sustainable over the long run (while they can go on for remarkably long periods of time, they usually come to an end at some point). This is because they completely depend on recruiting new investor money into the game to keep going. Since there is an entity siphoning money out of the investment pool, you have to constantly bring in greater fools to be able to pay out some investors. However, the supply of greater fools is not infinite. At some point, you run out of greater fools, and investors can no longer be paid out. Money continues to get siphoned out of the system until it collapses.

Real Life Example: Ponzi Scheme

A Ponzi scheme is a negative sum game for investors. First, there is only one source of money inflows (new investors). The only way investors can be paid out is through money from other investors. This would be zero sum, but the people operating the Ponzi scheme are siphoning some of the investors’ money. Thus, the pool of money to pay out early investors is less than what was put in. The operators of the Ponzi must continuously recruit new investors into the scheme to keep it going so they can keep paying the early investors and also so they can hide the Ponzi. These schemes can go on for long periods of time…Bernie Madoff’s Ponzi scheme went on for over a decade. Ultimately, though, they aren’t sustainable as new investors eventually dry up (assuming the Ponzi is not exposed before that).

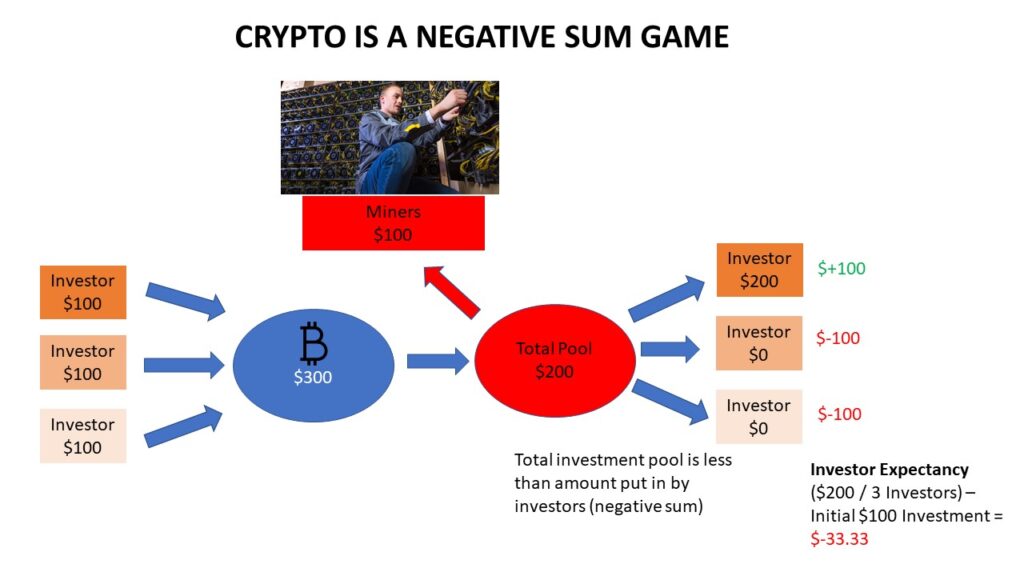

Real Life Example: Crypto

Crypto is a negative sum game for investors. First, there is only one source of money inflows (new investors). Unlike stocks, there is no underlying company with its own separate cash flows. Crypto tokens are just empty greater fool assets. Because there is only one source of inflows, crypto can never be positive sum. Anyone who makes money in crypto must be paid out by someone losing money in crypto.

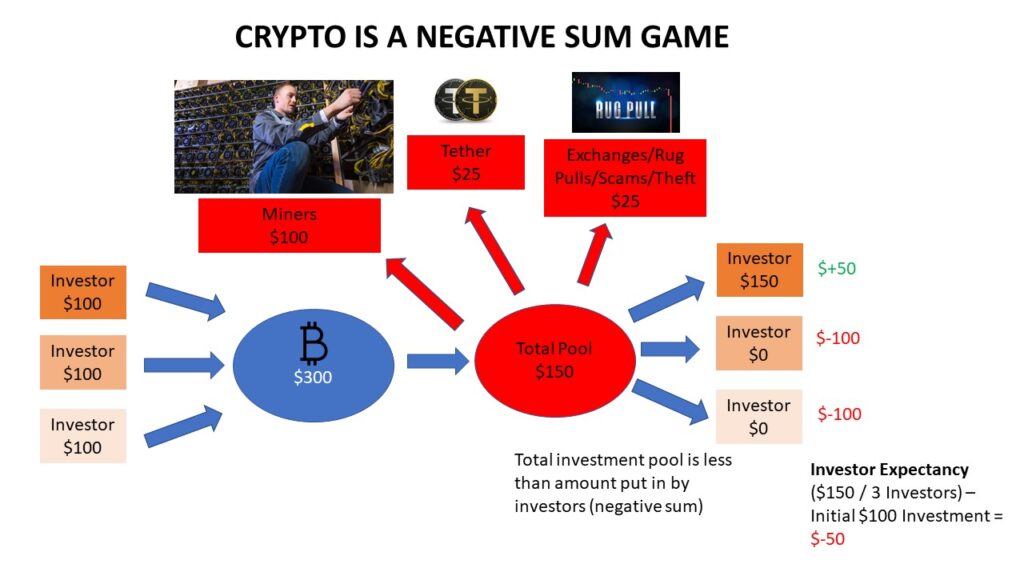

You might then ask, “Doesn’t that make crypto zero sum?” No. It is negative sum because there is an additional source of outflows: crypto miners. Miners are rewarded with crypto, and thus when miners extract crypto from the pool and sell crypto to pay their electricity bills, they are taking money out of that pool…the money investors have put in. Thus, the aggregate amount of money in the pool available to crypto investors is less than aggregate amount of money that was put in.

This is why crypto has often been compared to a ponzi scheme. They are both similar in money flows. They both have only a single source of inflows, and they both have a non-investor taking money from the pool. They both depend on recruiting new investors to keep things going. But they are both unsustainable because the pool of new investors is not infinite, and the system eventually collapses because investors keep competing for a smaller and smaller pool of money. In fact, crypto miners create the risk of the crypto miner death spiral (which would be a cool death metal band name), where the price of crypto falls below production costs and forces miners to sell (two such death spirals have happened in the past…December 2018 and March 2020). Estimates vary where that death spiral point is, ranging anywhere from $17K to $34K.

I’ve heard some people say, “Well, that’s just true for shitcoins. Bitcoin and Ethereum are great investments. They’ve been around the longest and have the most money in them.” However, all crypto tokens share the same negative sum structure. The market cap or age of the tokens is irrelevant. When you have a zero sum game of empty tokens that have separate entities (miners) extracting money from the investment pool, then it mathematically must be negative sum.

When you have a zero sum game of empty tokens that have separate entities (miners) extracting money from the investment pool, then it mathematically must be negative sum.

One person tried to tell me that she was invested in crypto for the long term, and thus it wasn’t negative sum. She thought that only the time frame mattered, comparing short term trading of stocks (zero sum) to long term index fund investing (positive sum). However, it’s not the time frame per se that changes the game you’re playing. The reason why long term investing is positive sum, while short term trading isn’t, is because with short term trading, the time frame is too short for a company’s separate cash flows to matter. For example, dividends don’t matter if you’re a day trader, but they matter if you’re a long term investor. You can also have instances where you initially invest in an unprofitable company (zero sum) that eventually becomes profitable and rewards shareholders with those profits (positive sum). Thus, holding for the long term in this case can transform a zero sum game into a positive sum game. With crypto, however, there is no underlying company and no separate cash flows. Thus, crypto will always be negative sum, whether you hold your crypto for 10 days, 10 months, or 10 years. You still can only make money by selling to a greater fool, and during all that time you’re holding, miners are continuing to extract money from the investor pool. Crypto is very much like a rigged poker game where a referee is constantly taking money out of the pot. And don’t let the large market cap or huge rise in price over the past few years fool you. The price of crypto is largely fictional, and winners can still only be paid out by multiple losers. The primary winners in crypto are whales who were in early, exchanges, and miners.

Crypto will always be negative sum, whether you hold your crypto for 10 days, 10 months, or 10 years.

And what about some of those crypto millionaires that you hear about, like the Dogecoin millionaire? Remember that since it’s a negative sum game, unrealized gains aren’t true gains. If someone hasn’t cashed out their crypto, they haven’t actually made any money (as of writing this, that Dogecoin millionaire guy still hasn’t cashed out from what I understand, and his unrealized profits have fallen substantially). The only way to make money is to cash out, which means other people will have to take the loss. But due to survivorship bias, you rarely hear about the losers, even though mathematically there will be way more losers than winners in crypto due to the negative sum nature.

Due to survivorship bias, you rarely hear about the losers, even though mathematically there will be way more losers than winners

Miners aren’t the only things that make crypto negative sum. The stablecoin Tether is used for approximately 70% of all transactions in the crypto ecosystem. You can think of Tether as casino chips; you trade your real $ for Tether, and then buy/sell crypto with Tether. However, the problem with Tether is that it’s not backed 1:1 by real money. Thus, the chips people are playing with don’t represent real $, which has been siphoned out of the crypto ecosystem and replaced with Tether. This is also why crypto prices are mostly fictional. For example, the current real price of Bitcoin as of writing this is not $36K in real dollars. It is below that; for example, GBTC, the Bitcoin trust that does not involve Tether, is trading at about 30% below NAV as of writing this.

Given that the crypto markets are unregulated, they are also full of rug pulls, scams, and front-running/manipulative tactics by exchanges. All of these contribute to the negative sum nature.

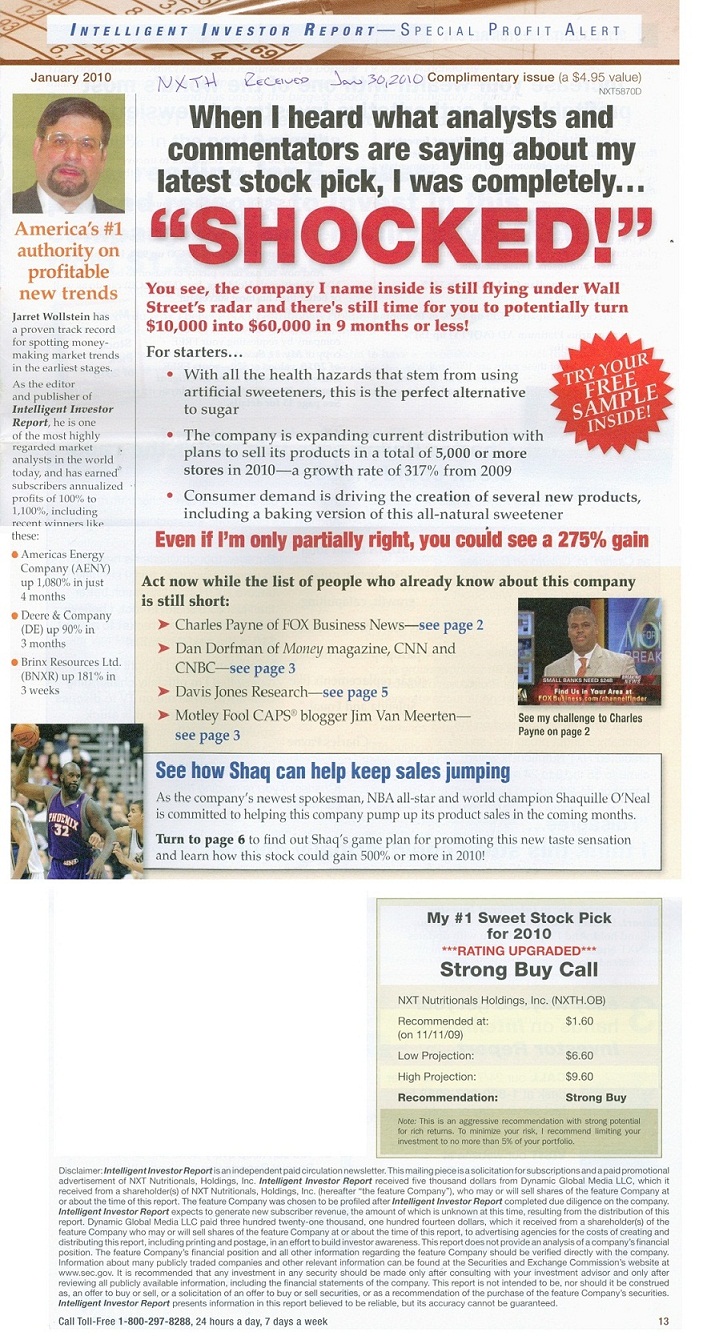

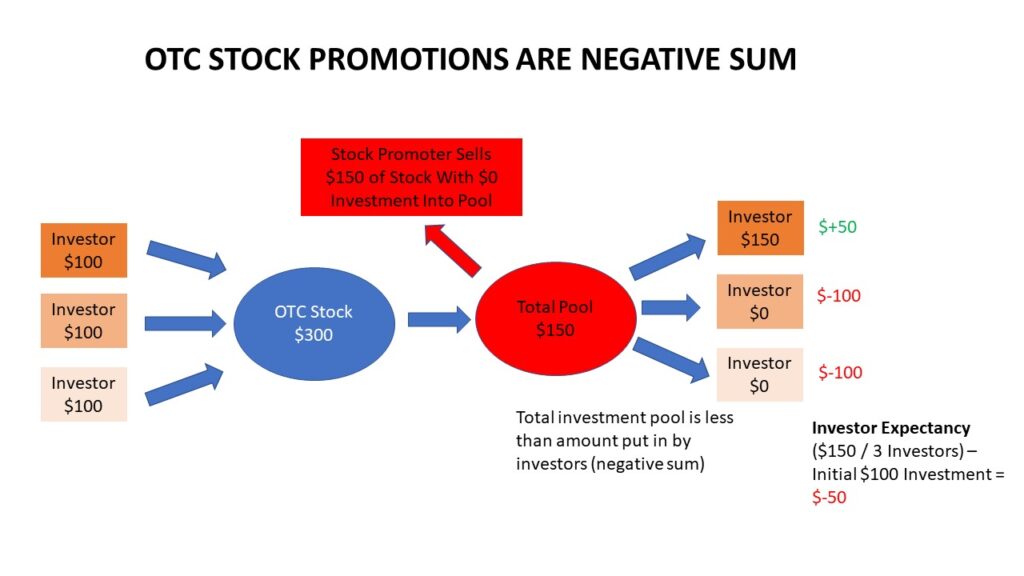

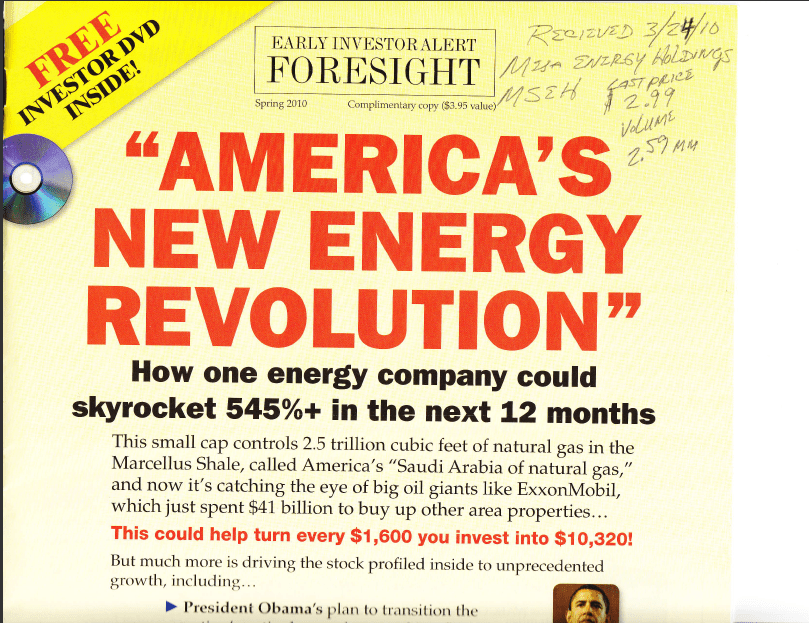

Real Life Example: OTC Pump & Dump Paid Stock Promotion

While you don’t see them much anymore due to SEC crackdowns, paid stock promotions were quite common on the OTC markets a decade ago. This is where a group of insiders, who have a large number of shares of a penny stock for no cost, pay for the stock to be promoted either through hard mailers or through internet ads. This paid stock promotion encourages people to start buying the stock.

– NXTH stock promotion mailer from January 2010

The stock promoters may also engage in manipulative trading techniques like wash trading (something that is also quite common in crypto … for other similarities between crypto and OTC penny stocks, check out my post here) to create the appearance of interest in the stock. People start to buy the stock. But who are they buying the stock from? The insiders who got their shares for free. Eventually, the insider finish selling their shares, and the stock promotion stops. Suddenly there is no one left to bid on the stock, and it collapses, leaving all of the retail holding the bag, while the insiders walk away with millions.

– JAMN stock chart from 2011. JAMN was an OTC stock promotion.

This is a negative sum game. Investors are putting their money into the stock. However, the insiders got their shares for free. They never put any money into the pot. They are only extracting from the pot. Thus, the insiders are being paid out by the investors. Yes, a few investors who are smart enough to exit before the dump can get out with a profit, but that only comes at the cost of another investor losing. In aggregate, the amount of money that investors can extract is much less than what they put in.

Know What You Own

The bottom line is that you really need to truly understand what you own. If you’re going to put your money into something, understand what type of game you’re playing, and act accordingly. Understand where money is going, and who the primary winners and losers are most likely to be. If you understand money flows and the game you’re playing, you’ll be more likely to make money and less likely to lose money. As the old saying goes:

God give me the strength to invest in positive sum games, trade zero sum games, and avoid negative sum games, and the wisdom to know the difference.

– Moi

Disclosure: Due to the negative sum nature and system risks in the crypto ecosystem, I have a small MSTR short and some long-dated BITO puts. I am also an InvestorsUnderground affiliate and receive a commission for anyone who signs up for their services through links on my site.

You’ll often hear traders talk about “conviction” on a trade, and even mention sizing in when conviction is high.

But should conviction dictate your trading decisions?

Defining Conviction

Conviction can be defined as “a strong belief or opinion” or “the feeling of being sure that what you believe or say is true.” Now, there’s nothing wrong with having conviction when entering a trade. Often, it is conviction that causes you to take the trade in the first place. You have a strong opinion that a trade has a high probability of working in your favor, so you decide to take the trade.

However, conviction can also cause problems when taking a trade, particularly after you’ve placed the trade.

The Problem With Conviction

Because conviction represents a strong belief, that belief can cause you to overlook evidence that the trade isn’t working, or that your trade or investment thesis is not correct. You can get stuck in confirmation bias, only looking for evidence that you’re correct and ignoring evidence that you’re wrong. Perhaps you’re so convinced the trade or investment will work that you put in a ton of size on it, risking more than you usually would. Or perhaps you decide not to obey any stop losses because you have such high conviction.

In all of these examples, your conviction has simply become poor risk management and/or a choice to ignore reality. You are confusing conviction with what you want to happen. However, what you want to happen may not be what is happening. And you can watch your money bleed away before your eyes as you let your conviction overtake you.

The $AMC apes/WSB army are also an example of conviction gone wrong. There is still a group of bagholding $AMC shareholders that are convinced that $AMC is being manipulated, that the shorts will get squeezed any day now, that $AMC is worth much more than its current value, and there’s a big conspiracy against them. Yet they ignore the evidence right in front of their eyes that they simply chased a short-term squeeze and got caught in a bubble. The $AMC insiders (like the CEO Adam Aron) have taken advantage of them and sold nearly $1 billion in stock to these bagholders.

Always Assume You Can Be Wrong, Even If You’re Convinced You’re Right

Whether you’re an investor or trader, you must always assume you could be wrong on an investment or trade, and you need to plan accordingly. This can be done through appropriate position sizing, diversification, and/or stop losses. Even if you feel there’s almost no chance of you being wrong, you still should prepare as if you could be wrong. Crazy things can happen in the markets, and you should always be prepared for a black swan event. You never want one trade or investment to wipe you out, even if your conviction is high or if the chance of something bad happening is small. If anything, you must at least account for the fact that your timing might be wrong. For example, Michael Burry was right regarding shorting the housing market, but he was early and his investors at first wanted to withdraw their capital.

For me personally, I no longer let conviction influence my position sizing or planning on a trade. I still only risk 2% of my capital per trade, even if I feel 100% certain on something. This is important, because keeping my risk at a fixed level allows me to be more objective about a trade. There’s an emotional component to conviction, and you can lose objectivity if your conviction is high. Interestingly, I’ve had some trades in the past where I didn’t have high conviction, and made great profits, and also other trades where I had high conviction, and ended up taking a loss. But in all those cases, I followed my trading plan and didn’t let my conviction level influence that plan.

I’m even starting to do long-term shorts again (despite swearing them off in the past). However, I’m much smarter about how I do them. I keep my risk fixed, I’m careful about my entry timing, and I view them as just another trade so that I don’t get emotionally involved in them. For example, I’m currently short the crypto markets through a small MSTR short and some BITO and MARA puts. My conviction is high…the crypto markets including Bitcoin & Ethereum are an unsustainable bubble, there’s massive systemic risk, and there is limited upside with tons of downside for a variety of reasons (including negative sum ecosystem for investors, lack of widespread use cases beyond speculation, extreme leverage, Tether fraud, and unsustainable energy consumption…you can read my reasons in more detail here, here, here, and here…also read the link list towards the end of the first one). However, despite my high conviction, I still use the same position sizing and risk management that I would do for any other trade. This keeps me stoic and indifferent about the eventual outcomes of these trades. Also, while I’m 100% certain I’m right about what will eventually happen to crypto long term, I can’t be 100% certain about the timing so I still need to manage risk.

Signs that Conviction Might End Up Blinding You

You don’t have any risk management in place. This could be not having a stop loss or using too much size in a trade or investment.

You think you can’t be wrong. No matter how convinced you are, remember that there still may be chance you’re wrong (remember the potential for Black Swan events), especially if you’re ignoring evidence contrary to your trade/investment thesis (more on this later). Also, remember that even if you’re 100% right on a trade or investment thesis, your timing could still be wrong. For example, if you’re convinced something is a fraud, remember that frauds can go on for long periods of time. Bernie Madoff’s fraud went on for 16 years, despite some people calling fraud in the 1990’s. The Wirecard fraud went on for 8 years, despite some journalists calling fraud very early on. Also, remember that the market can stay irrational longer than you can stay solvent. Bubbles, pump & dumps, and irrational market behavior can last much longer than you think they can.

You ignore or dismiss evidence contrary to your trade or investment thesis. This can be as simple as ignoring the price action telling you you’re wrong on your timing. Or, for a longer term trade or investment, it might mean ignoring evidence of problems with the trade or investment. For example, the $AMC apes have long ignored the massive insider selling, or have ignored the facts that their concepts of “naked shorts” are simply wrong. Or, I’ve seen crypto critiques dismissed as “FUD” despite very strong evidence of numerous issues within the crypto ecosystem (such as the Tether fraud).

Your identity is getting wrapped up in your investments or trades. For example, the $AMC apes have their own website like it’s a club. Or there’s the recent trends on Twitter for Bitcoin investors to have “laser eyes” in their profiles, or ethereum investors to add “.eth” to their Twitter names. Letting your identity become your investments or trades is a sure- fire way to lose objectivity about those investments or trades.

You get emotional with every swing of your investment or trade, and spend too much time watching it. Good traders/investors tend to be more stoic regarding how their positions go.

Would You Rather Be Right, or Would You Rather Make Money?

If you’re more focused on being “right” about your trade or investment, then that’s a sign that you’ve let conviction overtake you. Every trade or investment should just be one among many trades or investments. Don’t place too much importance on any particular one. Also, don’t get so caught up in trying to be right that you end up losing too much money if things go south on you. One hallmark of any good trader or investor is risk management. For traders, that means cutting losses when they’re small and not taking position sizes that are too big. For investors, that means staying well diversified, not sinking too much into any one investment, “knowing what you own” (and I mean truly knowing it…a lot of people think they know what they own but really only have a surface level of knowledge), and paying attention to your original investment thesis and being open to change your mind if that thesis might be invalidated.

Prepare, perform, profit, my friends…

DISCLOSURE: In addition the long dated MARA/BITO puts and MSTR short mentioned earlier, I have a small long term TSLA short and SARK (short ARKK fund) long.

2021 was an interesting trading year for me. It was a year I started off with a bang and ended with a whimper.

It was my best year ever in terms of absolute $ profits. However it wasn’t my best year in terms of percentage returns on my capital. Also, pretty much all the money I made in 2021 was made in the first three months of the year. I spent the rest of the year mostly flat. Now, this isn’t out of the ordinary for trading. I read a stat somewhere that profitable traders typically make most of their money on only 20% of trading days per year. This stat, in fact, highly influenced my risk management the past three years, and encouraged me not to worry if I had relatively long periods of time when I was flat. The profitable days will come, so manage your risk and make sure you keep the profits you make by regularly paying yourself. I’ve continued that practice, paying myself a salary from my trading profits every 2 weeks, and putting those profits away in lower risk long term investments. I also withdraw more if I’m struggling or in a drawdown to protect my capital. I did this in 2020 when I was in the middle of a 50% drawdown, withdrawing a huge chunk of my capital and shrinking my overall account size. I did it again this year when I experienced a similar drawdown. In fact, this year I paid myself about 70% of the profits I generated. Being a good trader isn’t just about making money…it’s about keeping the money you make. You can’t call yourself a good trader if you can’t keep the profits you make.

Being a good trader isn’t just about making money … it’s about keeping the money you make.

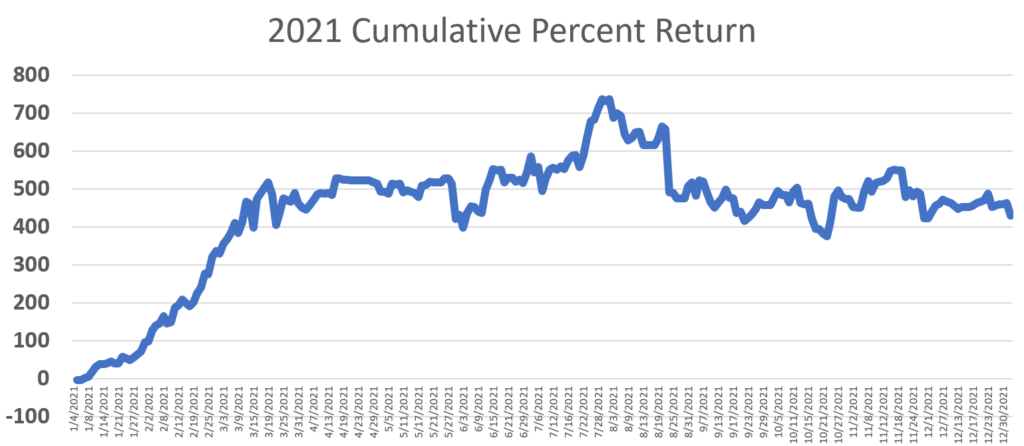

Here’s a graph of my cumulative percent return for 2021. You can see how I made all of my money from January through March, then had ups and downs for the rest of the year to finish mostly flat.

Overall, I finished with a 431% return on my capital. Here’s a summary of stats for 2021:

Cumulative % Return

431%

Average Daily Return

0.77%

Largest Drawdown (Peak to Valley)

-50.7%

Largest 1-Day Drawdown

-21.9%

Largest 1-Day Increase

16%

% of total trading days that were green

51%

% of total trading days where account hit all time highs

18%

Total Number of Trades

758

Winning Trade %

52.1%

Ratio of Gains to Losses

1.33

Win/Loss Ratio (Average Winning Trade/Average Losing Trade)

1.23

Max Consecutive Winners

11

Max Consecutive Losers

7

So why would the year start off so well but then end in a whimper? There’s a few reasons. First, two of my best strategies are shorting gappers and multiday parabolic runners, and there were TONS of these opportunities in January and February. Thus, my profitability was influenced by the sheer number of opportunities available. Second, in the summer I had such a big cushion for the year that I decided to experiment with new trading concepts and strategies. For example, I started experimenting with selling call options (call credit spreads) after reading many Twitter posts by @team3dstocks. Initially I had a lot of success with them, but then it started to fall apart. It eventually lead to my biggest drawdown of the year in August when I got auto-exercised on the sold call option portion of the spreads on TSLA and AMC when I misunderstood the process of what happens when part of your credit spread expires in the money (up until that point all of my spreads had always expired out of the money). I ended up with massive short positions in both, and they both gapped up the following Monday. I took huge losses on both in combination with a $3 million margin call (no, I didn’t lose $3 million…that was just the amount of money needed to cover the margin of the trade). Fortunately I was able to take a liquidation strike and not have my account restricted from trading on margin.

I also experimented with some changes to my existing strategies, as well as other newer concepts like the VWAP Boulevard concept that @team3dstocks had mentioned. I took a lot of lumps while working on these.

By November, I had tossed out most of the newer strategies that I had tried, keeping the few that seemed to have an edge. This is typical for trading. You’ll test out numerous strategies and spend tons of time on them, but eventually you’ll only find a few that really work for you. For example, after testing 10 trading concepts, you might only find 2 that really work. Because of this, trading is one of those activities where you can do a huge amount of work often with little to show for it, because you’re spending so much time evaluating strategies that eventually don’t pan out. The funny thing is that out of the various strategies I tested, the few that I’ve kept were just variations of my existing strategies anyway.

…trading is one of those activities where you can do a huge amount of work often with little to show for it, because you’re spending so much time evaluating strategies that eventually don’t pan out.

Even though in November I was done trying to experiment with new strategies, I still struggled to get any upside momentum going in my accounts because there were still weaknesses that were cropping up in the newer concepts that did have an edge. For example, for one newer strategy, I had some losing streaks that revealed a problem with the strategy. Those losing streaks would result in adjustments to the strategy which will enhance profitability over the long term, but in the short term my performance is adversely affected. Whenever you have a new trading strategy that looks good, be rest assured that the market WILL expose its weaknesses at some point. Every time I’ve thought I had a newer strategy “dialed in”, the market would come around and tell me that it wasn’t. Often, the tweaks that were needed were fairly minor too…sometimes just a minor tweak would stop a losing streak of 3-4 trades in a row without missing out on most of the profitable trades (like even just a time of day adjustment). But the only way to discover these weaknesses is through data collection and getting as large of a sample of trades as possible.

Whenever you have a new trading strategy that looks good, be rest assured that the market WILL expose its weaknesses at some point.

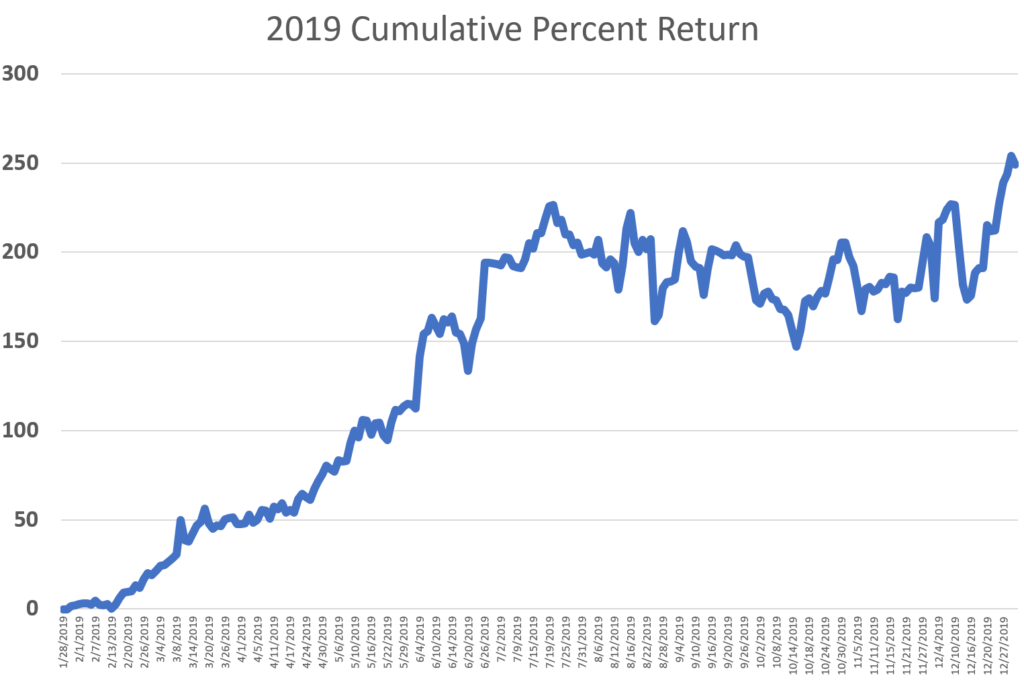

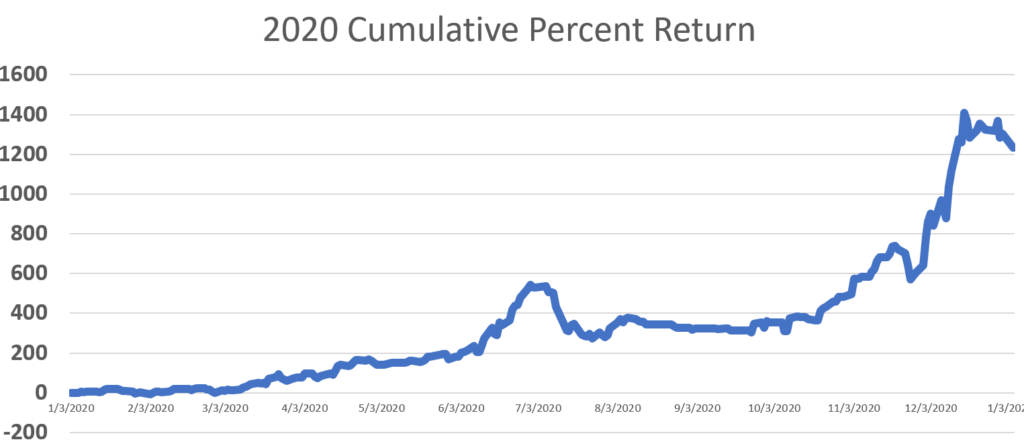

Here’s a year-over-year comparison of my performance.

2019

2020

2021

Cumulative % Return

294.2%

1233.3%

431%

Average Daily Return

0.59%

1.17%

0.77%

Largest Drawdown (Peak to Valley)

-22.5%

-51.5%

-50.7%

Largest 1-Day Drawdown

-15%

-16.3%

-21.9%

Largest 1-Day Increase

+15.5%

+18.9%

+16%

% of total trading days that were green

54.7%

50.2%

51%

% of total trading days where account hit all-time highs

26.7%

22.9%

18%

Total # of Trades

643

1098

758

Winning Trade %

61.9%

52.7%

52.1%

Ratio of Gains to Losses

1.40

1.46

1.33

Win/Loss Ratio (Average Winning Trade / Average Losing Trade)

0.86

1.31

1.23

Max Consecutive Winners

17

12

11

Max Consecutive Losers

12

21

7

You can see similarities in some stats among the years. For example, one similarity between 2020 and 2021 was a big 50% drawdown in the late summer. In both instances, they were caused by me experimenting with new strategies. In 2020, it was me repeatedly trying to do a long term short on $GSX. You can also see that 2020 was my best year in terms of % returns, but of course I made more absolute $ in 2021 simply due to having grown my accounts much larger.

My Trading Goals for 2022

Given these stats over the past few years, and the causes of my ups and downs, here’s my goals for 2022:

Focus on my existing strategies and avoid trying any new strategies. It was trying new stuff that was responsible for big drawdowns in both 2020 and 2021. I can make a lot of money with my existing strategies…there’s no need to add more. Just stick with my existing strategies and refine them if needed.

If I do have a new strategy in mind, don’t rush into trying it with real money after backtesting it. Paper trade it for a VERY long time. There’s no need to rush into trying a new strategy even if I think I’ve thoroughly backtested it. I can iron out the kinks with paper trading while making money with my proven existing strategies before I put any real money on the line with a new strategy.

Improve the efficiency of my trading. Focus on the best setups and improve my winning trade percentage. Make more with less. I’d like to be in the 70%+ winning percentage range, and focus more on setups that can give me a minimum of 2R per trade.

Eliminate the big drawdowns. Avoiding new strategies that aren’t thoroughly tested will help a lot with that.

Imagine a poker game. Imagine all the players putting their money in the pot, but only one player wins that money. It’s a zero sum game…one player wins, but the rest lose.

Now, imagine a referee for that poker game. His fee is to take money from the pot during each round. The game is now no longer zero sum for the players…it’s negative sum for the players because the amount of money that is available to the players to win is less than put in.

There will still be a winner in each game, but even though there’s a winner, it’s overall negative sum for the group of players involved. And for any person to keep making money, you have to recruit new players to play since some players will eventually lose their money.

Now, there’s another twist. The players aren’t putting cash into the pot. They exchange their cash for chips, and play with the chips. But unbeknownst to them, the casino taking the chips is pocketing some of the money, and thus the chips aren’t fully backed 1:1 by $.

Thus, the amount of chips that are being played isn’t reflective of the real $ that went in…there’s more chips than real $, meaning some players will get screwed when they try to cash in their chips. And hold tight, because it gets worse.

Some of the players have hidden cameras so they can see other players’ cards. This puts them at a distinct advantage over the other players. They consistently win more often, wiping out many players along the way (while simultaneously recruiting new ones).

On top of that, these players are in cahoots with the casino. They advertise how much money they’re making at this poker game. It’s the poker game of the future. They encourage others to play. But nobody hears about the players that are losing.

This game continues as long as there’s new players to keep playing the game. The small number of players with the hidden cameras or the most chips are able to just keep taking from all the new players. The games don’t stop until there’s not enough new players.

And remember, this entire time, there’s still a ref siphoning money out of the pot each and every game. So you’ve got a rigged game where there’s a few winners (the ref, a few players) and many losers (all the other players).

Would you play a poker game like this? Most would say no. But that’s the game you play if you invest in crypto. The miners are the refs. The crypto exchanges and whales are the players with a lot of chips or hidden cameras. The chips are Tether.

Keep this in mind whenever you think about putting your money into crypto. You’re playing a rigged poker game under the guise of the “future.” Eventually, it can only end one way for most players. No one can say when it will happen, but it will happen.

DISCLOSURE: Given the massive systemic risks in the crypto ecosystem, especially in regards to Tether, I own some long-dated BITO, MARA, and MSTR puts, as well as a small MSTR short position.

DISCLOSURE UPDATE 01/23/2022: I have closed out my long-dated MSTR and MARA puts. I continue to hold BITO puts and a small MSTR short position. I may re-enter new short positions on any crypto market bounce.

In 2011, while browsing Yahoo Finance, I was served an ad for Jammin’ Java.

However, this ad wasn’t for their coffee. It was for their stock.

Jammin’ Java was company trading on the Over The Counter Bulletin Board (OTCBB) under the ticker symbol JAMN. The company sold Marley Coffee … yes, a brand of coffee with Bob Marley’s name attached to it.

The internet was flooded with ads for JAMN. But the ads were focused on the stock, not the coffee. Now, there were some videos with Rohan Marley (Bob’s son) that seemed to be focused on the coffee, but even with those videos, they made it a point to show the ticker symbol for the company.

Why would a company that wants to sell coffee advertise its stock?

Because they wanted to hype the stock up so they could sell it at a high price, and let insiders get rich while leaving others holding the bag.

It was a classic OTC pump and dump campaign. But, rather than sending out hard mailers across the country to people’s mailboxes as had been previously done with other pump & dumps, the stock ads were primarily done on the internet.

The campaign was very successful. In early 2011, JAMN went from trading around 50K shares per day at a price of around 50 cents, to over 1 million shares per day. The stock eventually went parabolic, hitting a high of $6.35. And, like every other pump and dump, it would collapse and lose all of its gains.

JAMN now trades for .001 cents.

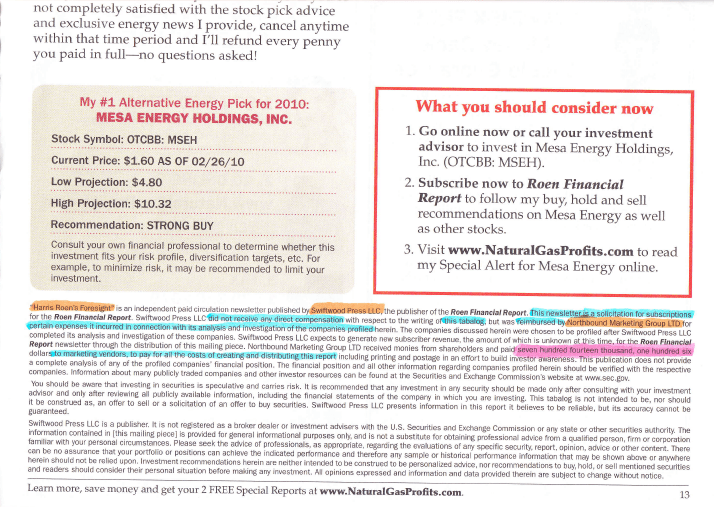

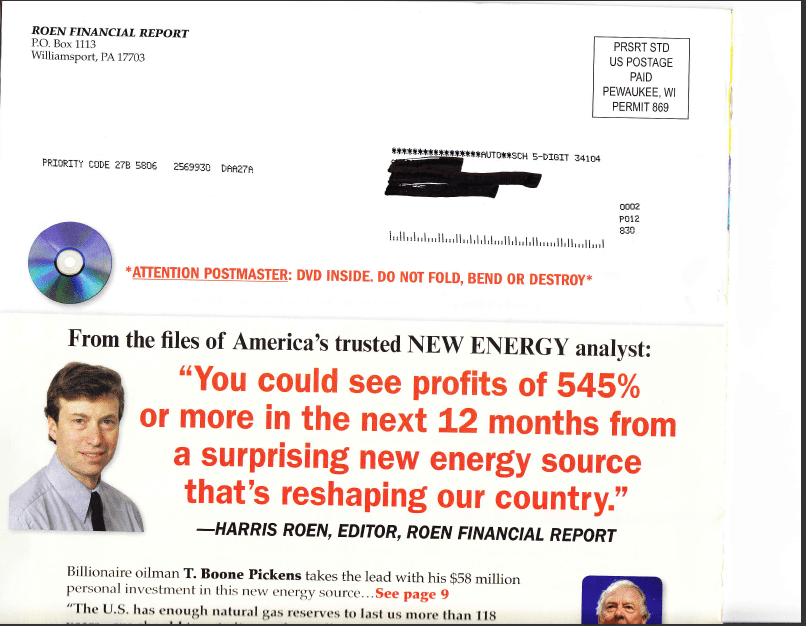

Before the SEC cracked down on OTC pump and dumps, they were common. I’ve even written about them in the past in their connection with the nutrition industry. One factor in common with all of them is they involved advertising the stock in some fashion. For JAMN, it was through internet ads. For many others, it was often through pamphlets or newsletters you’d get in the mail like these ones for MSEH:

Or this one for NXTH (which still trades for .005/share). This one even included Shaquille O’Neal in the pump.

You’ll note that all of these focus more on the stock rather than the company and its product. And that’s because the intent is to get you to buy the stock so that the people behind the paid pump could dump their shares (often which they had obtained for no cost at all) on you. The fine print would disclose that these were paid stock promotions, like this one for MSEH:

“Swiftwood Press, LLC…was reimbursed by Northbound Marketing Group LTD for certain expenses it incurred in connection with its analysis and investigation of the companies profiled herein….Northbound Marketing Group LTD received monies from shareholders and paid seven hundred fourteen thousand, one hundred six dollars to marketing vendors, to pay for all the costs of creating and distributing this report.”

But people usually don’t read the fine print.

Crypto: The New Paid Pump

You don’t see as many paid OTC stock promotions since the SEC has cracked down on a lot of them. But that hasn’t stopped paid promotions in general. They’ve just found a new home: cryptocurrency.

This was on the side of a London bus: an advertisement to buy Bitcoin.

The ads also appeared in the London Underground, and the ads eventually got banned. This also isn’t the first ad to get banned in the UK. Here’s another one encouraging investment in Bitcoin.

Full-page ads to get people to buy Bitcoin also appeared in Hong Kong tabloids. I wish I had screen captured them at the time, but I’ve been served Facebook ads in the past on Bitcoin.

And it’s not just ads for Bitcoin. It’s also ads for other crypto, like this ad with James Altucher.

Legit Companies Don’t Advertise Their Stock

Whenever you see paid ads promoting an investment, that’s a major red flag. The people promoting the investment aren’t looking to help you. They just want you to buy at a higher price. They’re playing the greater fool game, and they’re hoping you’re the greater fool.

They’re playing the greater fool game, and they’re hoping you’re the greater fool

Legit companies don’t advertise their stock. When I go to Costco’s website, I don’t get advertisements to invest in Costco. When I see ads for Target on the internet, those ads don’t tell me to invest in Target stock.

Why? They don’t need to. They have real products to sell. They make money through their business operations…not by selling stock.

Crypto is nothing like this. There is no underlying company or asset. Its only value is what someone else is willing to pay for it. It’s purely based on belief.

The Similarities Between OTC Pumps and Crypto

Crypto is more similar to the OTC pump and dumps. Here’s a list of the similarities:

1. LITTLE OR NO UNDERLYING BUSINESSES OR ASSETS

Most OTC pump and dumps were shells with no business operations. Of the ones that were business operations, they had little to no revenue and severe losses (JAMN had a cumulative 750K loss through April of 2011). Crypto is the same. There is no underlying business or asset for crypto. There’s literally nothing underneath it other than people’s beliefs.

2. PARABOLIC MOVES

Parabolic moves were common with really successful pumps. JAMN wasn’t the only OTC pump & dump to undergo a parabolic move and crash. Here’s LEXG from 2011.

Similar to the parabolic moves that some OTC pumps like JAMN and LEXG went through, cryptos have undergone parabolic moves and now in the midst of collapses.

3. LITTLE REGULATION

The OTC markets have much less regulation than the NASDAQ or NYSE, making them ideal for scams. This is similar to the crypto world, where there’s very little regulation which makes them a hotbed for scams.

OTC pump and dumps are a negative sum game for everyone but the stock manipulators. This means investors as a whole lose money. It has a negative expectancy for investors, meaning the average investor loses money.

This means that, just like the OTC pump & dump, crypto has a negative expectancy … the average investor will lose money on it.

This is very different from the stock market. The average investor who invests in index funds over the long term will make money and have a positive expectancy. It’s a positive sum game because the stock market is tied to economic output. There are real companies with real assets, cash flows, profits, and products underlying the stock market. That’s not true with crypto.

5. EXCITING LANGUAGE

If you look at the paid OTC mailers I showed you earlier, you’ll see a lot of language to excite you. Not only are there mentions of potentially large returns, but you’ll see words and phrases like “Revolution”, “the Saudia Arabia of Natural Gas”, “reshaping our country”, etc. They all promise that you’re getting in on the cusp of something exciting and new. Of course, these claims weren’t even close to reality.

The claims being made about crypto are no different. I’ve seen massive price targets put on crypto (like $250K for Bitcoin). I’ve heard crypto described as “revolutionary”, “disruptive,” “like the beginning of the internet”, “you’re getting in on ground floor”, “the latest technology”, etc. Of course, none of it’s true.

The emperor has no clothes, yet there’s a lot of people getting all excited about how good the emperor’s clothes look.

It’s not revolutionary or disruptive. “Blockchain” on which cryptocurrencies are based is simply technobabble for a type of encrypted decentralized database, and there’s nothing revolutionary about it. It’s not “disruptive” either. The last time I checked, Bitcoin, despite being around for 12 years, is only accepted by less than .01% of U.S. businesses (many of which are likely just crypto-related companies anyway). It’s extremely energy inefficient (currently, the average Bitcoin transaction takes enough energy to power a U.S. household for over 40 days…the same energy that it takes to do 1 million Visa transactions). It’s extremely slow (the Bitcoin network can only do around 7 transactions per second). The massive inefficiencies and energy consumption make them unscalable. The volatility makes cryptocurrencies unusable as currencies or as stores of value. They contribute to massive hardware waste. It’s unsustainable since the massive energy consumption only grows as the network and price go up. It’s also not like the beginning of the internet. From the 12-year period of 1992 to 2004, the internet showed rapid development and expansion to where EVERYONE was using it and it became a major component of everyone’s lives. In the 12 years of Bitcoin and all its crypto children, the only substantial changes have been in the prices, and the massive network energy consumption. I could go on and on, but there’s a massive gap between the supposed promises and language surrounding crypto and the reality. The emperor has no clothes, yet there’s a lot of people getting all excited about how good the emperor’s new clothes look.

I usually don’t care if people want to play greater fool or zero sum games. Hell, I’m a day trader which is a zero sum game at best. But, I’m very real with people when it comes to day trading. I tell them the stats that 80% of day traders lose money and less than 1% are able to predictably and reliably make money over the long run (which means that I’m in that 1%). I tell them it’s zero sum so that for someone to win, someone else has to lose. I usually warn people against getting into it, even though I day trade myself. And I tell them if they’re going to do it, prepare for a long, hard road before you get consistently profitable (if you ever do).

But people aren’t real when it comes to crypto. I don’t think your average Joe who has gotten into it is dishonest. I just think the person gets caught up in the excitement and emotions about it, and is unable to view it objectively. I think many aren’t aware of the risks (particularly the systemic risks), and/or downplay the risks and overestimate the upside if they do know about them (people in general have poor conceptions of risk/reward…look at the people who are willing to risk COVID but not get vaccinated). I think a lot of people also don’t know just how bad the energy consumption is, and if they do know, they have a tendency to greenwash it. I also think people don’t understand why it’s a negative-sum game.

I’ve gradually become more outspoken against crypto…moreso than your run-of-the-mill stock pump & dump simply because crypto costs all of us without giving us any real benefit. Its massive energy and hardware costs, carbon footprint, and enabling of ransomware (the Colonial pipeline ransomware attack was very costly) are serious problems. I’ve got no problem with people that want to speculate, but unfortunately this is an instance where people’s speculation are costing everyone else…not just the speculators.

I’m the type of person that, when I’m a neutral observer, I’ll read arguments from both sides to get a better idea of what’s going on. And every pro-crypto argument I’ve seen fails miserably. And the only pro-arguments I’ve seen for crypto come from people with a vested interest in it. So you need to ask yourself the question: who’s going to be more objective in their assessment of it? Would you believe independent scientists on the impacts of cigarette smoking on lung cancer, or tobacco companies?

I’ll note that I have friends who have invested in crypto in one way or another, so if you read this, this isn’t anything personal against you. But, just like in the fitness industry, I’m a skeptical, evidence-based person and the evidence isn’t in crypto’s favor.

…what has crypto actually done? What effect on society has it had, other than its ability to generate wealth for the wealthy and arbitrarily make a few others rich? What product has come out of crypto that you use? If crypto was to be entirely eradicated tomorrow, what hole would it leave in the average person’s life unless they’d put money into it?

If you want to read further on crypto, why the major arguments for it fail, scientific sources on its energy consumption, and the problems with stablecoins like Tether, here’s some sources (list updated 02/04/2022):

And this video is probably one of the most thorough educational videos on crypto, NFTs, and Web3 that you’ll find anywhere. It’s over 2 hours long, but has had 2.5 million views as of 1/27/2022.

Crypto-currencies are pyramid schemes designed to enrich the few on the basis of FOMO in the many

DISCLOSURE UPDATE 6/17/2021: When I originally posted this, I had no position in any crypto related instruments. However, given the extreme bubble and the high probability of a collapse of the crypto ecosystem due to a variety of factors, I now have some long-dated MSTR puts.

DISCLOSURE UPDATE 11/15/2021: Given the massive systemic risks in the crypto ecosystem, especially in regards to Tether, I recently decided to grab some long-dated BITO and MARA puts.

DISCLOSURE UPDATE 01/14/2022: Given the massive systemic risks in the crypto ecosystem, especially in regards to Tether, as well as the limited long-term upside and large downside risks to crypto, I recently decided to take a small MSTR short position. However, I may not hold it long term as it will depend upon the daily short interest I have to pay on the position.

DISCLOSURE UPDATE 01/23/2022: I have closed out my long-dated MSTR and MARA puts. I continue to hold BITO puts and a small MSTR short position. I may re-enter new short positions on any crypto market bounce.

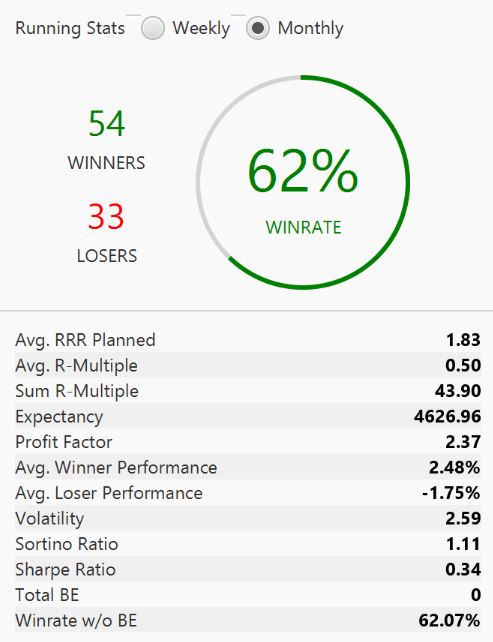

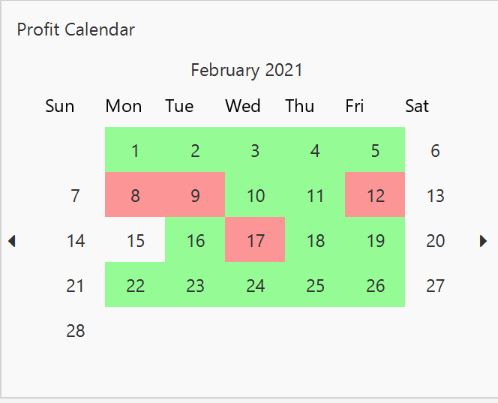

February ended up my best month in terms of absolute profits, and my second best month in terms of % return on my capital (122%) … just narrowly missing my best month of 124% in June 2020. It could’ve been better…I didn’t let some winners run enough, and I missed some what would’ve been really profitable trades. I wasn’t green every day, but I was green on most days. Approximately 6 out of every 10 trades were winners, and the size of my winners exceeded the size of my losers. The net gain on my winners was over twice the net loss on my losers. This is what I talk about when I tell new traders that they need to think like the casino and not the gambler. You need to have a statistical edge. You’re not going to win every trade. You’re going to have losing days. You will also have losing streaks. But if you have a statistical edge, you’ll make money over time. It’s not what you make in one trade. It’s what you make when you take 100 trades of the same setup. So do you have a statistical edge in your trading? If you don’t know, you need to start keeping a detailed journal. I generated these stats using Edgewonk, a trading journal that has a lot of cool stats to help you improve your trading.

Unless you’ve been living under a rock for the past week, you’ve probably at least heard about the GME/AMC debacle. It’s been framed as the common man beating Wall Street, the little guy beating the big guy, David vs. Goliath, the Rebellion against the Empire…

Except it’s none of those things. It makes for a good, gripping story, but, like Gary Taubes’s “Good Calories, Bad Calories” book (Gary is really good at coming up with compelling, yet false, narratives), it’s a story that just isn’t true.

The unfortunate thing is that false narratives have consequences. Gary’s false narrative leads people to an irrational paranoia surrounding carbs, a bad relationship with food, and potential struggles with weight loss when his “solution” doesn’t work. The GME/AMC false narrative perpetuated by Wallstreetbets and then spread through the echo chambers of social media has the consequence of causing a lot of people to lose money…some people who can’t afford to lose it.

Now, throughout this piece, some of you may read things you don’t want to hear. But that’s exactly why you need to hear it.

…throughout this piece, some of you may read things you don’t want to hear. But that’s exactly why you need to hear it.

THE TL;DR SUMMARY

If you’re too lazy to read this whole article, here’s a summary for you:

The restrictions placed on GME/AMC trading by Robin Hood and other brokers were not conspiratorial or corrupt in nature. They were necessary to manage the risk caused by the volatile stocks. The brokers and clearing firms were following regulations that have been in place since 1974.

The “little guy” didn’t win. Most little guys lost, and Wall Street won big. Only a few hedge funds with short positions lost.

Shorting is not “bad”, and the anger directed at short sellers is misguided.

GME/AMC became giant pump and dumps, and WSB orchestrated the pump.WSB did more to hurt the average Joe than it did to hurt Wall Street.

The market isn’t rigged against you.

The real reason most retail traders lost money on GME/AMC is because they showed the same bad habits that retail traders have had for years.

I’m not going to go into too much detail as to what happened. Gamestop (stock ticker symbol: GME) and AMC Movie Theaters (stock ticker symbol: AMC) made massive moves up to 1500% this past week due to a combination shorts squeeze/gamma options squeeze. The moves were initiated by a group of traders on the reddit forum /wallstreetbets. Both were heavily shorted stocks, with the hedge fund Melvin Capital and the well-known short seller Citron Research/Andrew Left having short positions. These funds were forced to close their positions which contributed to the massive move in the stock. If you want a more detailed explanation of the GME short squeeze/gamma squeeze, check out Sahil Bloom’s article on it (I highly recommend following his “Allegory of Finance” threads).

POPULIST RAGE

With these funds being forced to close their short positions, and with some WSB people now making money off the squeeze, the events began to take on a David vs. Goliath narrative. Wall Street was losing. The little guys were finally taking out those evil hedge funds.

Mr. Hedge Fund, don’t make me angry…you wouldn’t like me when I’m angry

The story took a conspiratorial turn when Robin Hood and other brokers restricted trading in the stocks due to the extreme volatility. This was viewed as the Big Guy changing the rules to stop the Little Guy from winning. The populist rage swept through the media. Even politicians started to get into the act, with calls for increased regulation. “Those corrupt brokers are in on it! The market is rigged against us!” said the little guy.

Suddenly, more and more people wanted to get in on the GME/AMC action. Everyone wanted to kick Wall Street’s ass now. “Let’s all herd together and buy more stock, forcing those evil shorts to cover more!” they yelled. I saw people on my FB feed now wanting to jump in. WSB became full of people exclaiming “Hold the line!”, encouraging people not to sell their positions. It was war.

Unfortunately, it was a war against the wrong people. It was a war based on misinformation and misconceptions of what was happening. And a lot of the little guys are now holding the bag.

Let’s get into all the misinformation and misconceptions, why the whole story was wrong, and why the suits won (spoiler alert: it’s not for the reasons you think).

ROBIN HOOD: TAKE FROM THE RICH, GIVE TO THE POOR, OR VICE VERSA?

First, let’s address the idea that Robin Hood was somehow conspiring with the suits by restricting trading in the stock. The reality is much less nefarious.

When you trade stocks through a broker with a margin account, you’re not the only one taking on risk. The broker takes on risk too, and there are regulations in place to make sure your broker manages that risk appropriately.

The decision by Robin Hood to restrict trading wasn’t due to some conspiracy with the suits. The restriction on trading happened across multiple brokers, not just Robin Hood. In fact, even some of those evil hedge funds were restricted from trading the stock. And there weren’t just restrictions from the long side. I wasn’t able to short GME at Cobra Trading because their clearing firm Wedbush wasn’t allowing shorts (I was able to short at Vision Financial, however).

The restrictions were necessary because the volatility had gotten extremely high. There were so many people with accounts trading these volatile stocks that the clearing firms didn’t have the cash to make sure that trades would be settled. Here’s an excellent explanation as to why Robin Hood and other brokers had to restrict trading in GMC and other highly volatile meme stocks.

Good explanation on today's trading halts by Robinhood and others in tonight's Closer. pic.twitter.com/N89T4Lw4bD

The fact is, Robin Hood and the other brokers were simply following the regulations that have been in place since 1974. There was no corruption or anything nefarious. Really, the restrictions on the stock were the fault of WSB and the masses of traders who created such massive volatility in the stock that put the brokers at risk. The WSB army didn’t hurt Wall Street, but it was starting to hurt the brokers that WSB traded through, and the brokers had to put a stop to it. WSB was biting the hand that fed it. And, as a result, WSB ended up hurting the retail traders.

WSB was biting the hand that fed it. And, as a result, WSB ended up hurting the retail traders.